Stable VN Dong, Despite the Iran War, Surging Inflation, and the Widening Trade Deficit

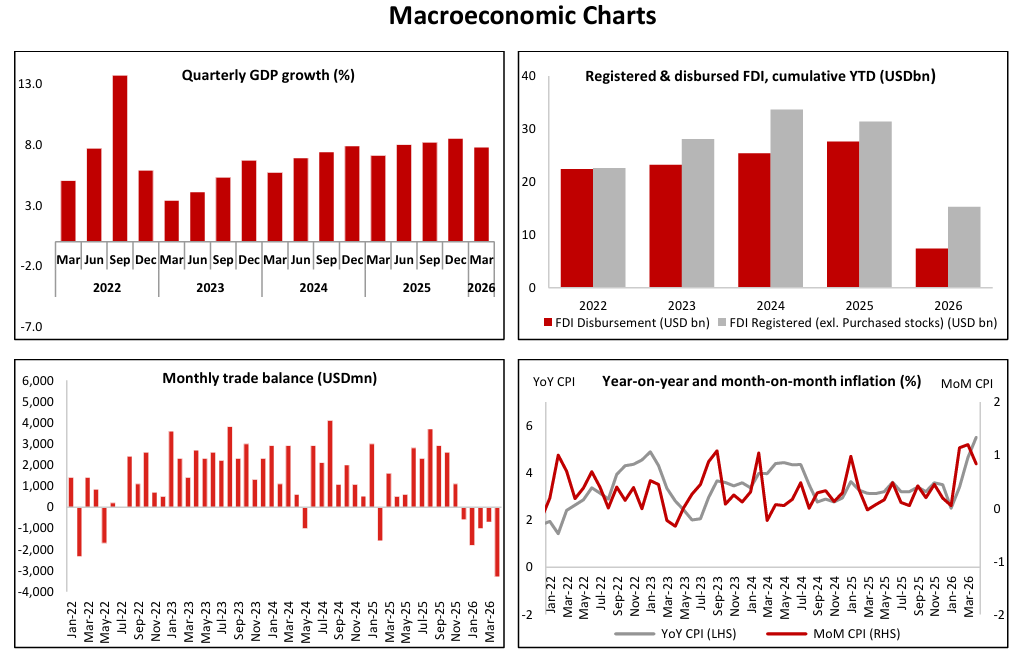

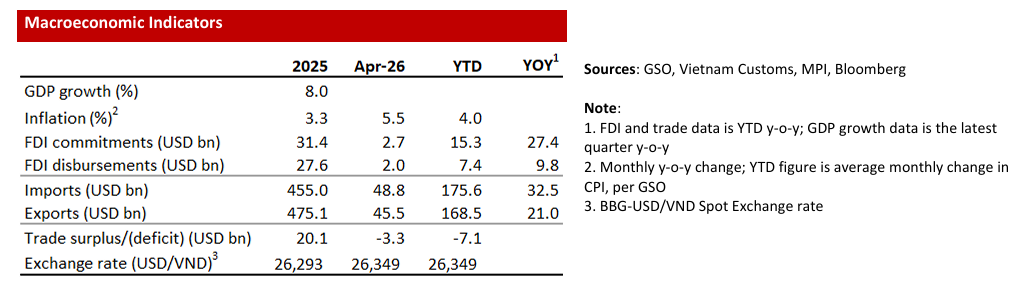

Increasing Inflation: CPI Inflation in Vietnam vaulted from just over 3% before the war to nearly 5% in March, accelerating to a 6-year high of 5.5% YoY in April. The sharp rise in Brent oil prices by more than 60% YTD in March (and April), would have pushed inflation in Vietnam up to around 5.5%, but the Government essentially began subsidizing petrol prices to the tune of over 20%, which limited headline CPI inflation in March. The subsequent acceleration of CPI inflation in April stems in part from the secondary effects of higher energy costs, especially from non-subsidized products such as diesel. However, residential rents in Vietnam surged in recent months for reasons not related to the war, which accounts for much of the acceleration in Vietnam’s inflation from March to April.

Widening Trade Deficit: Vietnam’s trade surplus widened from 3% of GDP (which is considered high) in 3M26 to 4.5% in 4M26, driven by a circa 60% YoY increase in Brent oil prices and a circa 6% YoY appreciation in the value of the Chinese Yuan, without which Vietnam’s trade deficit would be around 2%/GDP. Vietnam’s exports of computers and electronics surged nearly 50% in 4M26 (following a near 50% increase last year), but this surge is temporarily adding to the trade deficit because imports of production inputs – including capital goods – that are needed to support future tech product production are soaring.

Interest Rates Have Stabilized: Bank deposit rates (for 12-month deposits) rose by about 120 bps over the five months leading up to March but have now stabilized at around 7-8% on average. The driver behind the interest rate increase was that credit growth outpaced deposit growth by about 5%pts in 2025. However, the classic commodities-world adage: “the cure for high prices is high prices” is now playing out: those higher interest rates have driven a collapse in loan demand and a surge in deposits. Consequently, credit growth has only outstripped deposit growth by about 2%pts YTD and interest rates have stopped rising, although rates are likely to remain high in the months ahead because of the inflation surge.

Interest Rates and Residential Rents: Higher deposit rates pushed mortgage rates up to a point that has led to a collapse in demand from new home buyers and a jump in apartment rental demand. This dynamic, coupled with some other idiosyncratic factors that also put upward pressure on residential rents, were the key factors that pushed up Vietnam’s CPI inflation in April. Normally, we associate higher interest rates with dampening inflation, but in this quirky scenario — the likely temporary fall in home purchases driving intense rental demand — is pushing rents (and thus inflation) higher.

Stable VN Dong Exchange Rate: The higher trade deficit and surging inflation discussed above would typically put depreciation pressure on Vietnam’s currency, but the USD-VND exchange rate was nearly unchanged in April and is nearly flat YTD. That’s partly because the US Dollar/DXY Index fell by 0.6%pts in April, and the increase in VND interest rates is supporting the Vietnam Dong. Additionally, the global and Vietnamese economies have been more resilient than expected to the closure of the Strait of Hormuz.

Update on Our Views About the War’s Impact on Vietnam: We had expected the closure of the Strait of Hormuz to start

creating problems for Vietnam’s economy around the time of the publication of this report (which we discussed here).

However, there has been nearly no impact thus far, and we are pushing back the time horizon in which significant problems could arise if the Strait is not reopened to July due to both global and local factors. We are not oil experts, but in our understanding, the consensus from experts such as Goldman Sachs and others that the world economy would start to have major oil problems around now was predicated on estimates of: 1) circa 1m barrels-per-day (bpd) of demand destruction vs actual demand destruction of circa 5m bpd, and 2) Chinese oil inventories of circa 1.3 billion barrels at end-2025, whereas the actual figure was probably closer to 2 billion.

That last point closely relates to the “oil diplomacy” that China has undertaken, doling out some refined products to countries in the region. China, as well as Japan, both see it as in their own interests to keep Vietnam’s energy needs well-supplied because both countries have invested so much in factories here. Consequently, Vietnam’s vulnerability to this oil crisis is probably much less than initially expected (especially because of China’s much higher than previously estimated oil reserves), and some of the details reported about discussions that took place during the recent visit of Japan’s Prime Minister to Vietnam, also reinforces our belief in this assessment.

Finally, while April was quite eventful, our views on the war’s impact on Vietnam’s economy has not changed over the last month. We still expect 7% GDP growth this year, which would make Vietnam one of the fastest growing countries in the world this year.