Record High Trade Deficit in 5M26

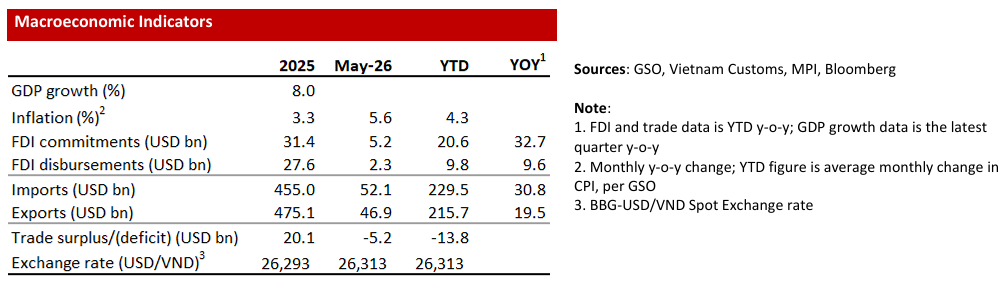

Stable VN Dong, Despite Record Trade Deficit: Vietnam’s trade deficit more than doubled from 3% of GDP pre-war (versus a 4%/GDP trade surplus last year) to a 7%/GDP trade deficit in the first five months of the year, driven by: 1) the US-Iran War, which has pushed crude oil prices up more than 50% this year, and 2) the AI boom, which pushed memory chip prices up more than 100%. Despite Vietnam’s surging trade deficit (anything over 3% is considered large), the USD-VND exchange rate was nearly unchanged in May and year-to-date, in sharp contrast to many of Vietnam’s EM peers, including Indonesia, which was forced to hike rates twice in the past few weeks to protect that country’s currency.

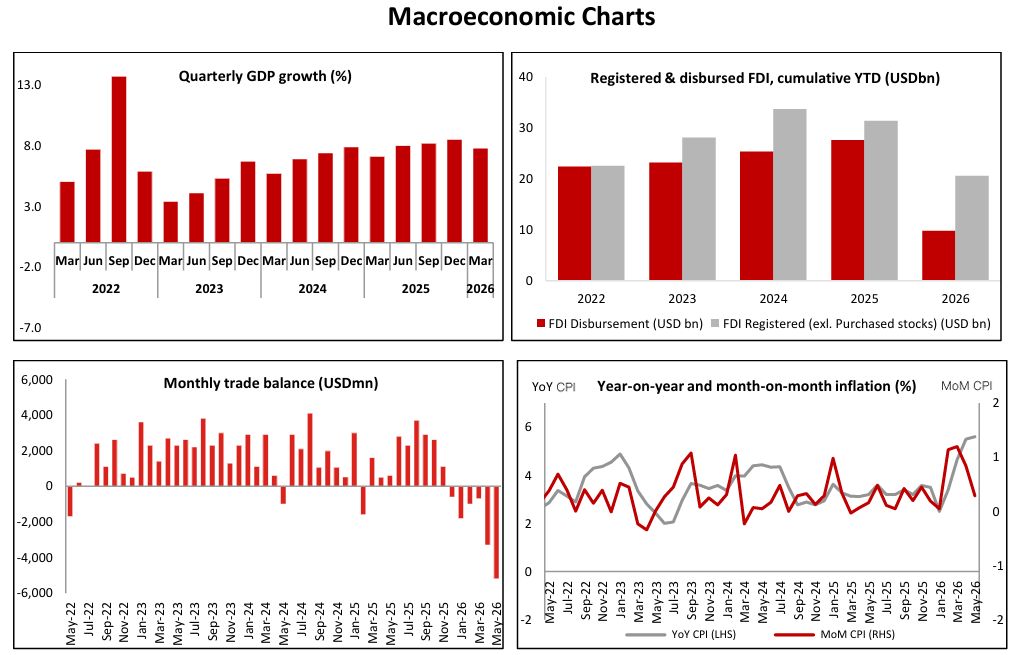

The War and the Trade Deficit: Vietnam’s imports jumped by a stunning 31% YoY in 5M26, far outpacing exports, which grew by a still-respectable 20% YoY. The resulting USD 13.8b trade deficit is a record high for the first five months of any year in Vietnam (for context, Vietnam’s full-year trade deficit reached USD 18b in 2008). Of that 31% import surge, about 5%pts is attributable to surging oil prices and Chinese Yuan appreciation, both of which are related to the war (see here). In short, Vietnam still would have suffered a circa 4%/GDP trade deficit even if the war had not happened due to the AI boom.

The AI Boom and the Trade Deficit: Vietnam’s electronics imports increased 57% YoY in 5M26 as FDI companies imported a very high volume of inputs required to produce AI-related products. However, the AI boom pushed up the prices of those inputs – especially of memory chips. Our rough, “back of the envelope” estimate is that surging memory prices account for about 8%pts of Vietnam’s 31% total import growth in 5M26, while imports of electronics components contributed another 14%pts, and the war added another 5%pts.

Manufacturing Driven GDP Growth: Vietnam’s manufacturing sector is the primary engine of the country’s growth this year, growing 9.5% in 5M26, driven by the production of high-tech products (Vietnam’s computer and electronics exports grew by nearly 50% in 5M26, after having surged nearly 50% last year). In contrast, real retail sales growth (i.e., consumption) actually decelerated from 6.7% in 2025 to 6.1% in 5M26 while tourist arrival growth normalized from 20% last year to 15% this year. At the beginning of 2026, we expected consumption growth to start picking up and manufacturing growth to start leveling off by mid-2026, but so far, we see signs of neither. Manufacturing is being driven by the AI boom, while consumption is being held back by poor sentiment and high mortgage rates.

High Interest Rates Are a Double Edge Sword: We mentioned above that the USD-VND exchange rate has been surprisingly stable despite Vietnam’s 7%/GDP trade deficit this year. Furthermore, the VND has shrugged off USD 2b of foreign sales of Vietnamese stocks this year, following USD 5b last year which we discuss in this report. In short, 12-month bank deposit rates are up more than 100 bps YTD to circa 7-8%, which is above Vietnam’s 5.6% YoY CPI inflation rate in May, and which is supporting the value of the VN Dong. That said, those high rates are filtering through to prohibitively high mortgage rates of around 13-14%, which is dampening consumer sentiment and spending.

We Expect Fiscal Stimulus in H2: The Government set very ambitious GDP growth targets at the beginning of 2026 and more-or-less reiterated its formidable aims despite the war. Infrastructure construction is surging, which is good for the country’s long-term economic growth as well as supporting growth in the short-term. However, the boom has skyrocketed construction materials prices and workers’ wages, limiting the likelihood of a further infrastructure spending surge in H2. For that reason, we expect significant Government fiscal stimulus in H2 to boost consumer spending. In short, we continue to expect 7% GDP growth this year – which would make it one of the fastest growing countries in the world in 2026 – but that expectation is contingent on aggressive, additional stimulus measures to support consumption and for the US-Iran war to be resolved in the next few weeks.