Continued Weak Consumption, Strong Manufacturing

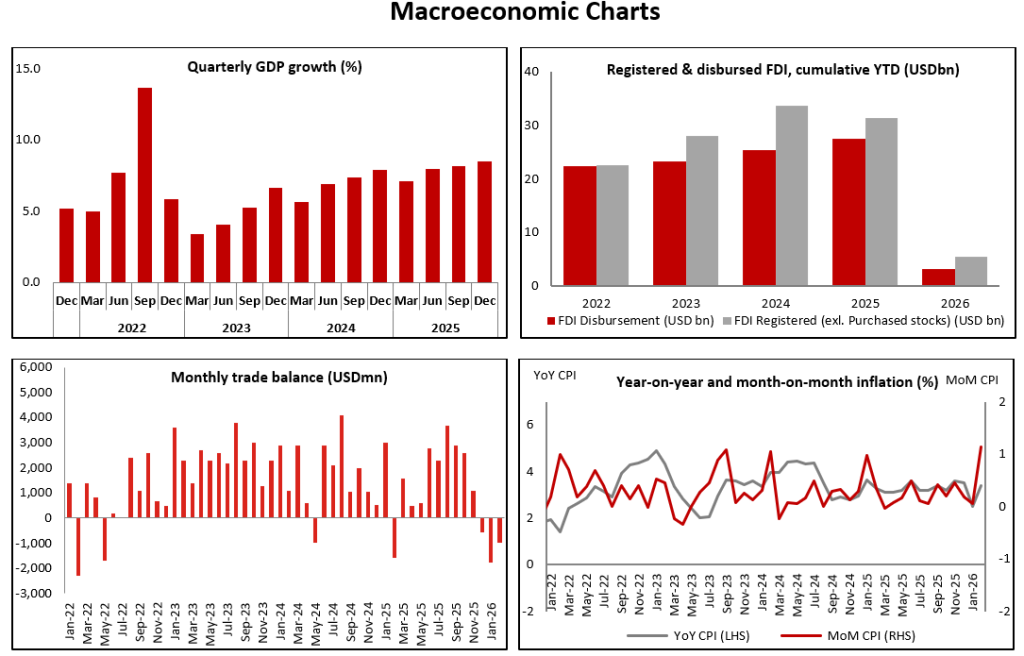

The economy has started 2026 on an unexpected trajectory. In the first two months of 2026, Vietnam’s manufacturing output significantly accelerated, but consumer spending softened, which is the opposite of the trajectory we had expected for the year. In 2025, Vietnam’s economy was driven by a surge in exports of high-tech products to the U.S., which boosted manufacturing output, and by a rise in tourist arrivals—especially from China. Consumption by local consumers was lukewarm last year, and we had expected a continuation of those conditions in the first half, followed by a pickup in the second half as consumers rebuild their savings buffers, post-COVID.

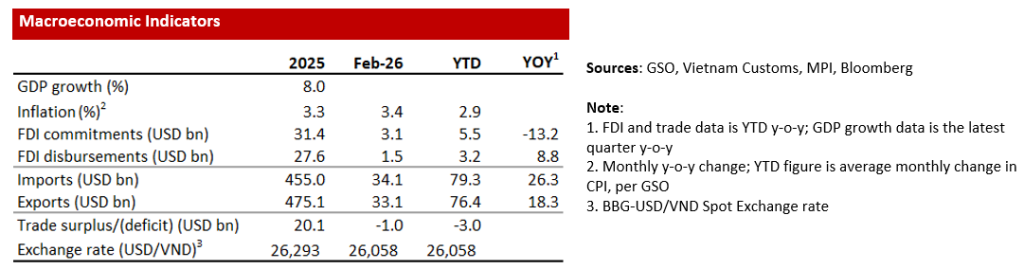

Manufacturing accelerates, tourism growth moderates. We also expected “soft landings” for both the manufacturing and tourism sectors. Instead, manufacturing accelerated from 10.5% growth in 2025, to 11.5% yoy in 2M26, pushing Vietnam’s manufacturing PMI up from 52.5 in January, to 54.3 in February while Retail Sales growth fell from 9.2% in 2025, to 7.8% yoy in 2M26 – although the deceleration in tourism arrival growth is playing out in line with our expectations, decelerating from 21% to 18%.

Continued strong exports to the US. Insatiable demand by U.S. consumers for high tech products that are made in Vietnam has delayed the soft-landing scenario, which we still expect later this year. Vietnam’s exports to the US and exports of computers and other electronics products grew by 22% and 41% respectively in 2M26. Furthermore, imports of production materials by FDI companies soared – which is a strong leading indicator (total imports surged 26% yoy in 2M26, versus 18% export growth). However, new export orders have flattened out, and the US-Iran war should dampen US demand for Vietnam’s exports somewhat – although our base case for the war will end up being a short, sharp conflict, which we discussed in this report.

Higher interest rates weighing on consumption. Bank deposit rates in Vietnam increased by about 1%pts last year (to 6% for 12-month deposit rates), and that increase is starting to filter into resettable mortgage interest rates (mortgages in Vietnam are floating rate and typically reset every two years). Rates on many mortgages are now resetting from ~10% to ~13%, which is one factor dampening consumer sentiment and spending. Notably, some articles have already highlighted weaker spending during this year’s Tet holiday.

What will the Government do? Vietnam’s Government has a 10% GDP growth target for 2026, including a 9% target for Q1. Consumption is over 60% of GDP and manufacturing is 25%, so the dip in retail sales growth from 9.2% to 7.8% is only partly offset by the acceleration in manufacturing output growth from 10.5% to 11.5%, which implies GDP growth slipping from 7% in 1Q25, to about 6.5% in 1Q26. This weak performance, coupled with the negative impact of the US-Iran war (which is likely to knock at least 0.5%pts off 2026 GDP growth) means that the Government will need to take decisive actions in order to achieve an acceptable level of economic growth.

Limited options to boost growth. Coming into this year, the State Bank of Vietnam signaled its intention to tighten credit growth limits in 2026 – partly to protect the value of the VN Dong. Those measures worked. The USD-VND exchange rate has barely moved this year, despite a circa 5% increase in the US Dollar/DXY Index, in the lead-up to the war. The surge in oil prices means that inflation in Vietnam will likely spike from 3.4% yoy in February to over 5% in March and April, before dropping alongside oil prices once the war ends, which will impede the Government’s ability to support GDP growth by cutting rates. The Government could also double down on infrastructure spending but spending already surged by more than 40% last year, and physical limitations impede how quickly additional spending could flow into the economy.

Measures to support consumption. Given all the above, we believe that the only realistic way for the Government to boost GDP growth is by taking aggressive measures to boost consumption and/or the real estate market. Last year, the Government took actions to boost consumer sentiment and spending, including a modest personal income tax break, a slight VAT reduction, and severance payments to laid-off civil servants, but given that cutting interest rates aggressively amid increasing inflation is not realistic, the most obvious path forward would be for the Government to pursue more aggressive measures to stimulate consumption, potentially, including support tied to the housing sector (this is just our speculation on what could be done, but any effective measures to support the economy would likely target real estate and consumption support).