War Impact Begins to Hit; K-Shaped Economy Emerges

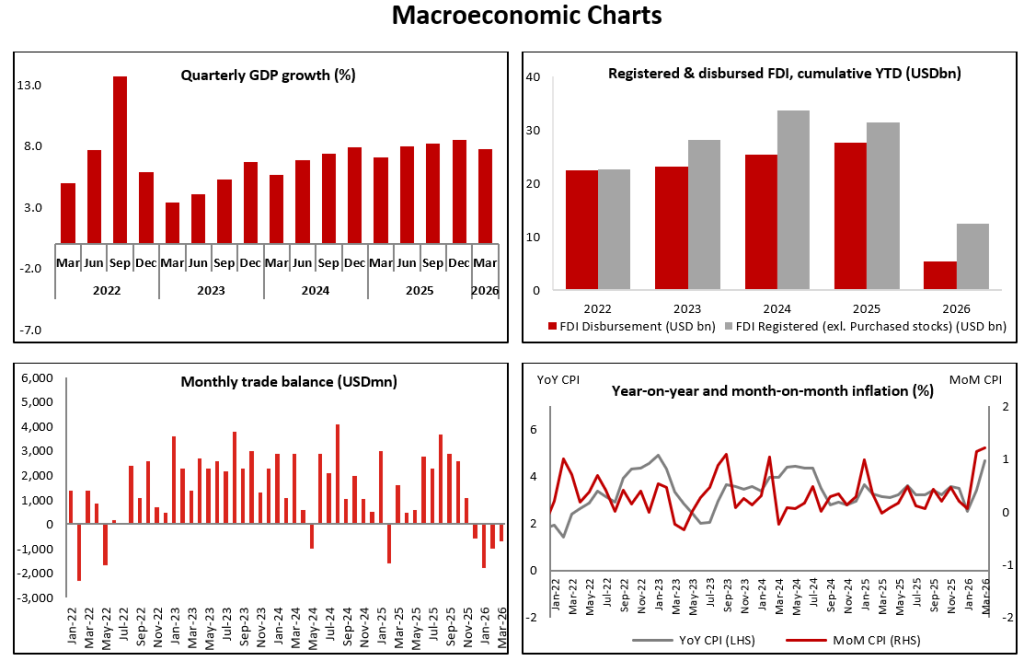

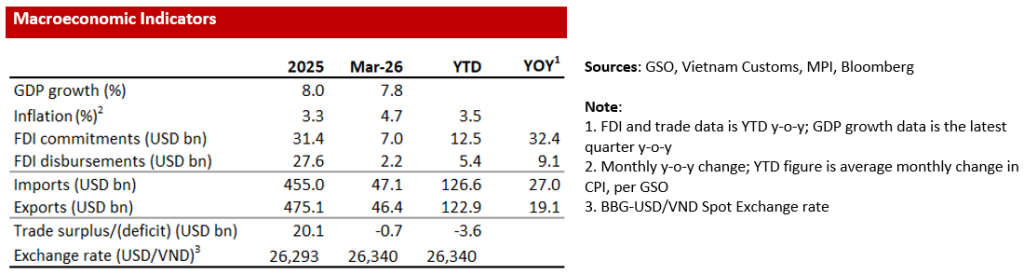

War Risks Shaving 1% Off Vietnam’s 2026 GDP Growth. We expect the US-Iran war will reduce about 1%pt from Vietnam’s 2026 GDP growth, based on the assumptions that 1) the Strait of Hormuz is re-opened soon (which we discussed in this report) and 2) Vietnam’s Government takes concrete measures to mitigate the impact of the war on the economy. That said, the war’s impact only started hitting some parts of the economy in March rather than having uniform, across-the-board ramifications. For example, CPI inflation in Vietnam immediately surged from 3.4% YoY in February to 4.7% in March, but the Q1 GDP growth figures the Government reported remained resilient.

Solid Q1 Growth Despite War. Vietnam’s National Statistics Office (NSO) reported that GDP growth dipped from 8% in 2025 to a still very robust 7.8% YoY growth in Q1 2026, and that real retail sales (meaning retail sales excluding inflation) actually accelerated from 6.7% in 2025 to 7% in Q1 2026. That acceleration is surprising, considering that tourist arrival growth in Vietnam fell from 20% in 2025 to 12% YoY growth in Q1 2026, which reduces real retail sales by nearly 1%pt, ceteris paribus. In addition, the NSO also revised up the 2M26 retail sales growth figures by 2.5%pts, which is the biggest upward revision in our memory.

K-Shaped Economy Emerges. One explanation for these idiosyncrasies is the emergence of a “K-Shaped Economy” in Vietnam. The concept stems from the letter “K,” with an upper and lower part, symbolizing the divergence: consumption remains robust among upper-middle-class and upper-class consumers, while those at the lower end are facing more difficulties. We have often discussed the K-Shaped Economy in the US, which supports Vietnam’s exports; and which explains why Vietnam’s consumption picture is marked by sharp divergence across segments. Specifically, anecdotes vary considerably depending on which segments we look at: consumption of products and services upper-middle-class consumers can afford are more robust than staples for the working class, which complicates the job of the Government statisticians.

High-Tech Exports Mask an Impending Manufacturing Downturn. The output of the manufacturing sector (circa one-quarter of Vietnam’s GDP) also remained very resilient in Q1. Manufacturing output growth dipped slightly from 10% in 2025 to 9.7% in Q1, supported by a continued increase in high-tech exports to the US, including laptops and electronics. In Q1, electronics exports were up 46% YoY, total exports to the US rose 24%, and Vietnam’s PMI remained above the ‘50’ expansion-contraction threshold for the ninth consecutive month. Despite that strength, there are clear leading indicators that these figures will drop in the months ahead.

Export Rollover Acceleration. We were already expecting a rollover in Vietnam’s exports this year, as the US restocking cycle was nearing an end (high-tech exports to the US jumped nearly 50% last year), and Vietnam’s new export orders had already started falling slightly, but the war will dramatically accelerate that dynamic. Vietnam’s Manufacturing PMI number dipped from 54.3 in February to 51.2 in March, driven by that shrinkage of export orders, a surge in input cost inflation to its highest level since COVID (which will squeeze profit margins), and a plunge in the employment sub-index of Vietnam’s Manufacturing PMI, which dropped from 53.2 in February, to 46.1 in March, after having been in a fairly tight range over the previous five months (around 51-53).

Interest Rate and FX Rate Risk. The average 12-month bank deposit interest rate in Vietnam climbed by roughly 50 basis points to nearly 7%, with some banks offering rates above 8% during the second half of March. This surge was partially driven by banks’ quarter-end statutory liquidity requirements. Next, the USD-VND rate depreciated by a modest 1.1% MoM, despite the 2.4% jump in the DXY index last month. To stabilize sentiment in the FX market, the SBV sold nearly USD 2.8bn in 6-month “cancellable” FX forward contracts and targeted illegal gold and crypto activities in order to curb speculation and demand for USD in the unofficial market.